Don't be suckered by this number

CAP rate is the go-to metric in real estate investing. You'll see it everywhere online once you start looking. It's ubiquitous because it's one metric that can be compared across any property. Realtors use it all the time. Like a box of matches, in experienced hands it's a useful tool. In inexperienced hands, it can burn your house down. I'll show you why.

What is CAP rate? I wrote a detailed post on the definition (see below). Simply put: it is the money you make after all running costs divided by the purchase price. It's analogous to yield on a bond.

Say the annual rent on a place you're considering is $20,000 and the bills you (not the tenant) would pay are $5,000 (think property tax, gas, maintenance, water/sewer, snow removal etc.). The property has a net operating income (NOI) of $15,000 per year. And say the place is listed for $300,000, then the CAP rate is $15,000/$300,000 or 5.0%. That's the headline number you will see in online listings like at www.loopnet.com.

CAP rates don't included your personal circumstances like whether you use a property management company, or if you'd increase rents, or your financing costs, or your tax bracket and so on. That's the seduction of CAP rates: they're specific to the property and not to you or me.

But CAP rates don't tell you anything about:

- The tenant quality you might attract

- The vacancy rate you might experience

- The building or land condition you might need to deal with

- The capital appreciation you might achieve

- The ease in selling the property in future (liquidity)

CAP rates don't account for risk

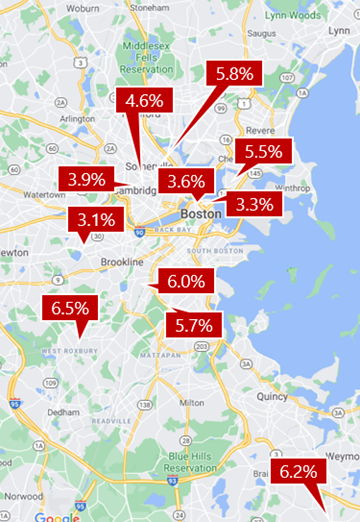

CAP rates for multifamily units around Boston

Source: loopnet.com

And that's the key. A higher CAP rate is a riskier property and a lower CAP rate less risky. CAP rates are usually lowest close to gentrified downtown areas and increase as you move further out.

I can unscientifically demonstrate the CAP-rate-vs-distance phenomenon in Boston. As of writing this there are ten multifamily units within a narrow price band for sale showing their advertised CAP rates. CAP rates are almost never above 4% in downtown Boston. 2-3 miles outside of Boston - the wealthy neighborhoods of Cambridge and Brookline excepted - CAP rates jump to around 6%.

Moving from 4% to 6% CAP rate is like saying you can get 50% more net operating income for an equivalent purchase price!

You don't have to have lived in Boston to know the downtown core is a dense place with a lot of activity. There are many reliable, good credit, urban professionals willing to rent or buy. In other words - COVID-19 notwithstanding - it's a low risk area today. The low risk attracts low risk buyers who are willing to bid up prices and, like a bond, drive down CAP rates.

As a property investor you're trying to find the right risk/reward property profile for your financial objectives. Use CAP rates carefully as one input into your overall decision. It isn't the perfect number people pretend it to be.