'Commercial' is closer than you think

You might think "I'm just starting out, no-one will say I'm a 'commercial' investor".

Not so fast.

There are three triggers that will make your property a commercial investment.

- Your investment multi-family property has five or more residential units in it.

- Your investment property has at least one office, retail store, or some other rental unit that is not residential.

- You have more than four (typically) investment properties with mortgages attached.

The last one is interesting.

Once you have more than four investment properties with mortgages, banks will likely consider you a 'professional' real estate investor. Your next investment property - even a modest single family home for rent - will likely be considered commercial. (Technically you can have up to ten properties, but banks get understandably skittish much above three or four).

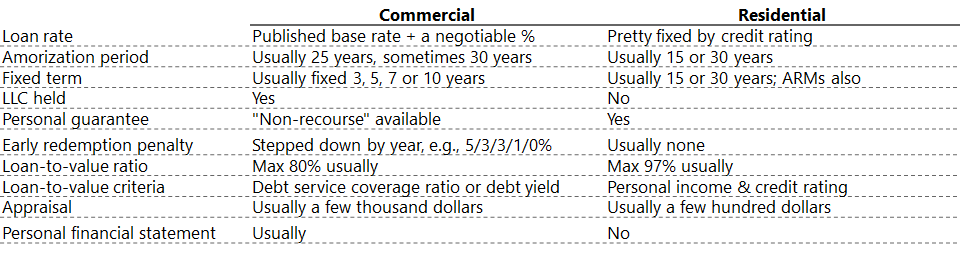

Residential and commercial mortgages are different. The first is paint-by-numbers. The second is a rough pencil sketch. You have few parts of a residential mortgage to negotiate. You have many more with a commercial mortgage.

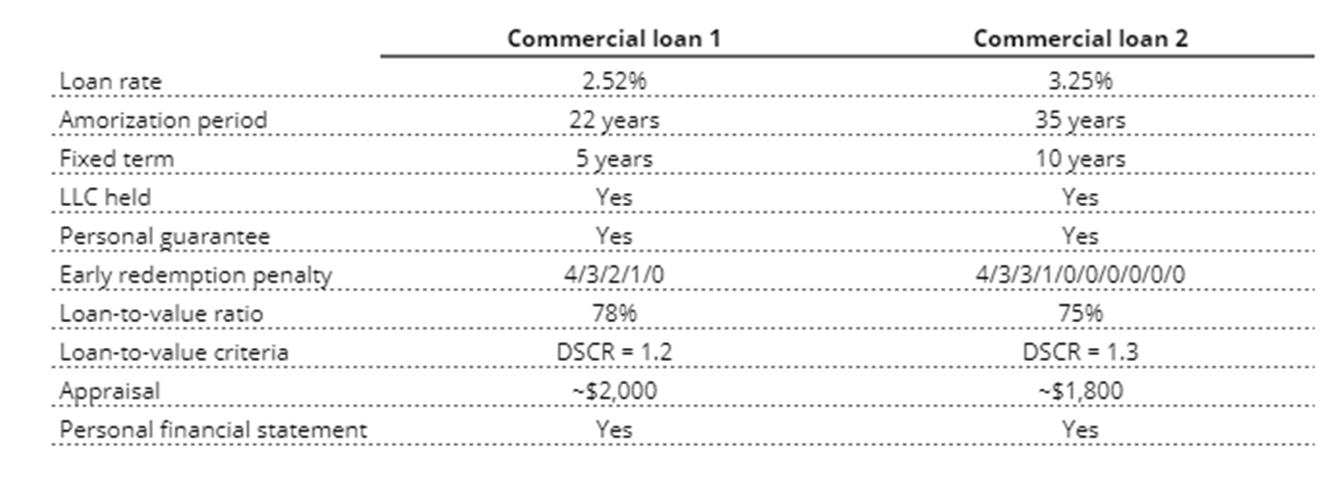

In the last three months I've negotiated two commercial loans. Here are the main terms:

Back in January I interviewed Nate, a senior commercial lender in New England. He touched on many of the differences between commercial and residential lending.

Laziest Landlord

Laziest Landlord

The first thing to realize is different bank employees - and different parts of the bank - manage residential and commercial loans. The tone of the conversation is different. (I am sure the compensation structure is different between residential and commercial sides). Residential feels like shopping for clothes at Target. Commercial is like shopping at a tailor.

I want to stress I haven't dealt with the big commercial side of banks. That seems to be a completely different beast. They deal with loans in the tens of millions of dollars.

What are the differences between the terms of a residential and commercial loan? What is negotiable and what isn't?

Differences between commercial and residential loans

The table is not exhaustive. There are exceptions. But it covers most of the major differences. Consult directly with your lender.

The three areas that I've found negotiable with commercial loans are:

- The % on top of the published base rate. I'm typically quoted rates of 140 bps to 200 bps over the federal home loan bank rate. Depends on the fixed term.

- The early redemption penalty. Banks seem to default to 5/4/3/2/1% for a five year term. That is, refinancing or redeeming your loan in the second to last year generates a fee of 2% of the outstanding loan balance. You might negotiate to 4/3/1/1/0% instead. It's an insurance policy for the bank and you can negotiate their fees.

- The debt service coverage ratio. DSCR is the total cash generated divided by the total cash costs. The usual ratio is 1.2 to 1.45. The higher the number, the more you'll have to put down. DSCR is a cushion for the bank (and for you).

I try and build and maintain relationships with a handful of commercial lenders. They want to know who you are. What your plans are. What your background is. Having 2-3 lenders you can run a property past before making a formal offer is invaluable.

Good luck on your commercial investing journey.