Why I'm buying during a pandemic

I bought my first rental unit at the bottom of the Great Recession. I'm in the process of buying a 3-unit rowhouse just as the second wave of COVID-19 escalates. Why?

There is, of course, the famous Buffett saying "be fearful when others are greedy, and greedy when others are fearful". People have undeniably moved out of larger cities because of COVID-19 and the ability to work remotely. The recent changes in rents in Toronto and San Francisco as extreme examples. Fear is in the air.

I have six reasons for buying during this pandemic:

- I have limited competition. Few investors are looking for multi-family rental units.

- Lenders are skittish to finance (read: they're looking for great credit), so the investor pool is further constrained.

- I've found low fixed rates. At the end of October 2020 rates were as low as 3.25% (see below).

- I believe people will return to quality, well-run cities with great amenities in the medium term.

- I've had my eye on a location in Boston that is low risk: gentrified, commuter lines, away from my other properties, 30 feet above sea-level (important by the coast!).

- I've secured a turnkey, full-tenanted property with rents already discounted for COVID-19 where the numbers work for me.

Here's the property I'm buying:

I opted to pay for a $980(!) home inspection to give me extra peace of mind given the other (COVID-19) risks. It's a four hour commitment to learn every little thing about the asset I'm buying. A great investment. Yes, it's money up front on a transaction that may not go through. I offset the cost by negotiating with the seller to contractually commit to fixing the issues.

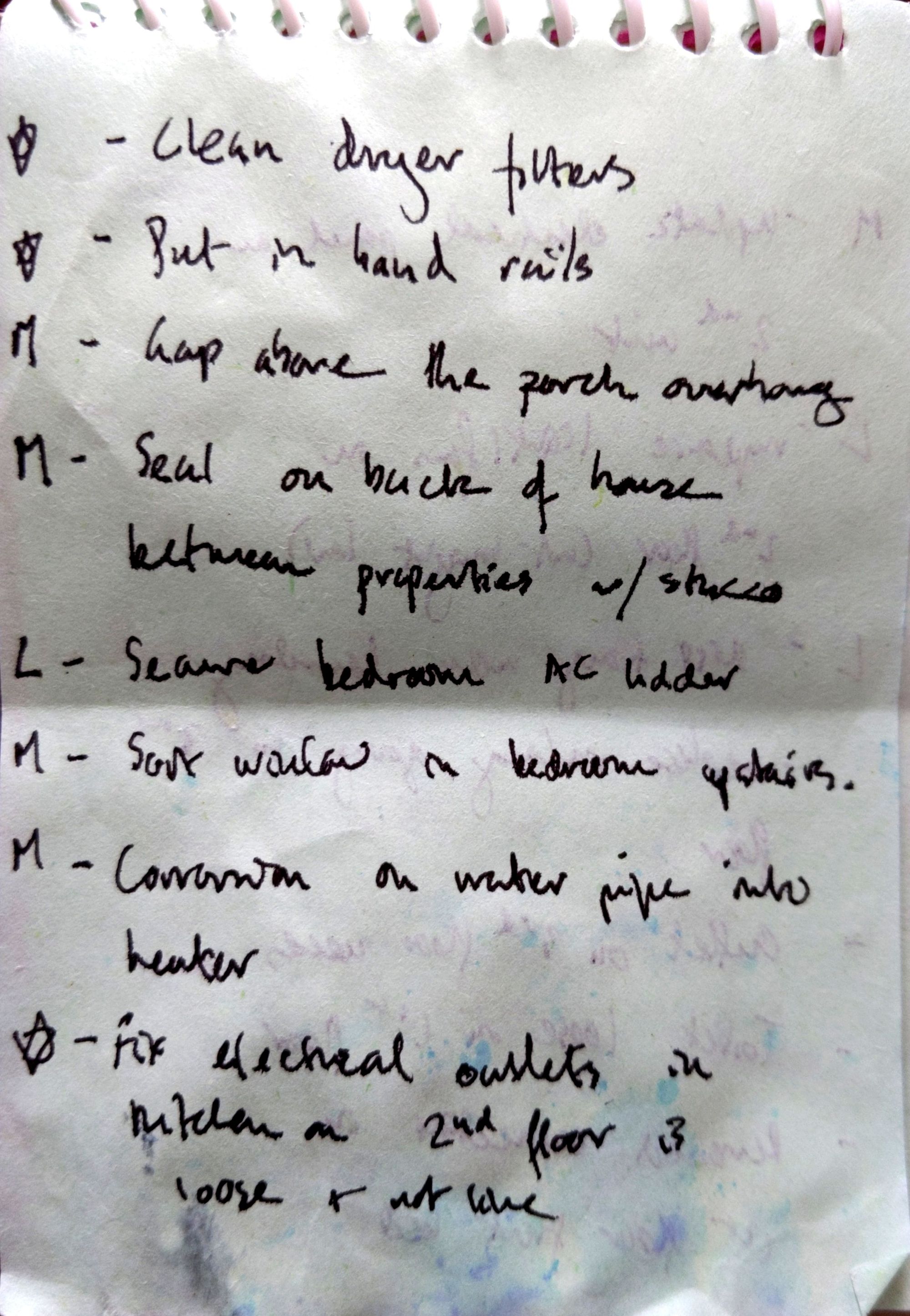

My own list of fixes & upgrades...

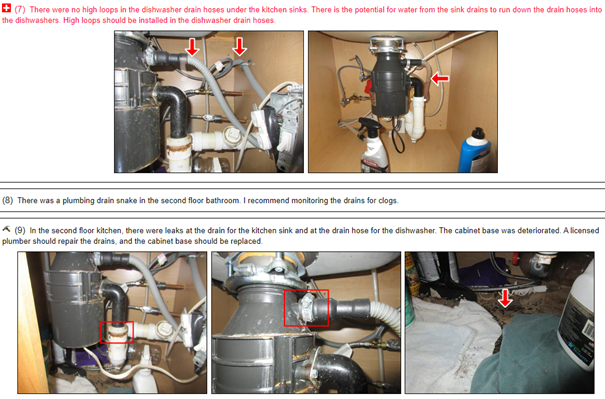

...along with the inspection report...

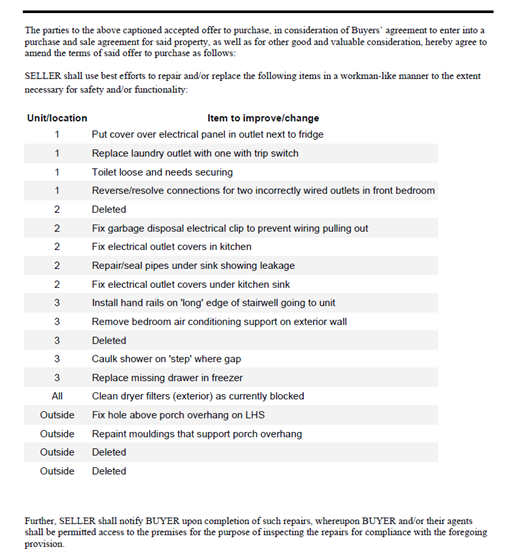

..made into an addendum in the P&S

I offered 4.3% less than the asking price and signed the offer to purchase at 3.9% under asking. With the already-reduced rents here's the 5 year returns proforma:

I try and balance being conservative and realistic in my proformas. Else the only person I would be deluding is myself. These numbers include:

- 1 week vacancy per unit per year (this might be a bit aggressive)

- Already discounted rents (about 10%-15% less than pre-pandemic norms) in year 1

- 3.5% fixed rate mortgage with just 20% down payment (confirmed with the lending bank)

- 0.3% annual maintenance/repair budget (given the current condition, this is about right)

- All other actual 2020 costs (insurance, water, taxes etc.) with 2-3% annual price increases and my usual property management costs of 3.5% on gross rents

The big jump in the financials between the 1st and 2nd year of ownership assumes I can raise rents to pre-pandemic levels. Even if I can't, this is a solid ROE with positive cash flow. And, as a rule, I never include capital appreciation or depreciation write-offs.

Should you invest during the pandemic too? I encourage you to think about your investment criteria like my six above. There's never a perfect time to invest. And there's no such thing as a bad property. Just a bad price.